Understanding the Rent vs Buy Decision

Deciding whether to rent or purchase a home is a major financial alternative that depends on the lifestyle, goals and financial conditions. Both options have different benefits and shortcomings, and understanding them can help you make an informed decision. To make a deep dive into this topic, find out if it is better to rent or buy a house.

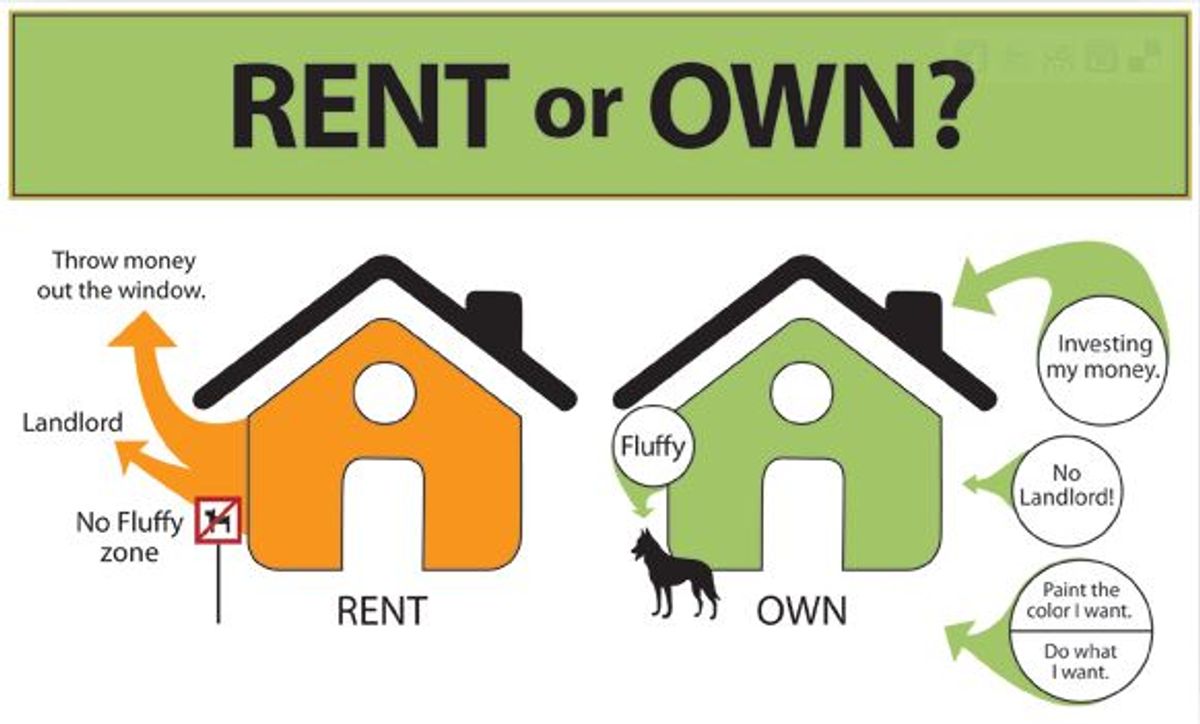

Benefits of Renting a House

The rent provides flexibility, which makes it ideal for those who can often move or do not prefer to commit to the same place. This usually involves low pre-costs, as tenants avoid payments and shutter fees. Maintenance and repair are often controlled by the landlord, which reduces unexpected expenses. Rent lets you live in desirable areas where purchases can be ineffective. However, the payment of rent does not build equity, and you can meet restrictions to customize your living space.

Advantages of Buying a House

Buying a house is an investment in your future, imparting the capability for belongings price appreciation and fairness increase. Homeownership provides stability and the freedom to customize your property. Mortgage payments may be comparable to rent in a few markets, and interest may be tax-deductible. However, buying requires sizable advance expenses, inclusive of a down payment and final fees, and homeowners are liable for renovation and maintenance. To weigh those factors, take a look at whether it is better to lease or purchase a house.

Financial Considerations

Your economic scenario performs a critical position on this selection. Renting may be better when you have confined financial savings or unsure profits because it avoids the monetary burden of a loan. Conversely, shop for experience if you have stable profits, true credit, and sufficient savings for a down payment. Consider housing marketplace tendencies—excessive home costs or hobby charges can also desire renting, even as low charges ought to make shopping for greater appeal. Calculate lengthy-time period expenses, along with belongings taxes and insurance, to decide affordability.

Lifestyle and Long-Term Goals

Lifestyle factors are equally important. If you affect mobility or estimate major life changes, it provides flexibility for rent. The homeowner plans to stay in one place for many years, as it takes time to receive the purchase costs again. Think about your priorities: would you be responsible for maintaining the house, or would you like it to be easy to rent? Adjust your choice with your career, family plans and personal preferences.

Making the Right Choice

To decide, evaluate your financial readiness, market conditions, and personal goals. Use online calculators to compare renting and buying costs over time. Consult with a financial advisor or real estate professional to understand local market dynamics. Whether you choose to rent or buy, ensure the decision aligns with your current needs and future aspirations. For more insights, visit is it better to rent or buy a house.